Paper 04 · 7 min read · April 28, 2026

What we don't trade — and why.

Discipline isn't the trades you take. It's the ones you skip. Four setups the data pushed us to cut from the playbook, and the cost of taking them anyway.

Class A solo

Net-negative

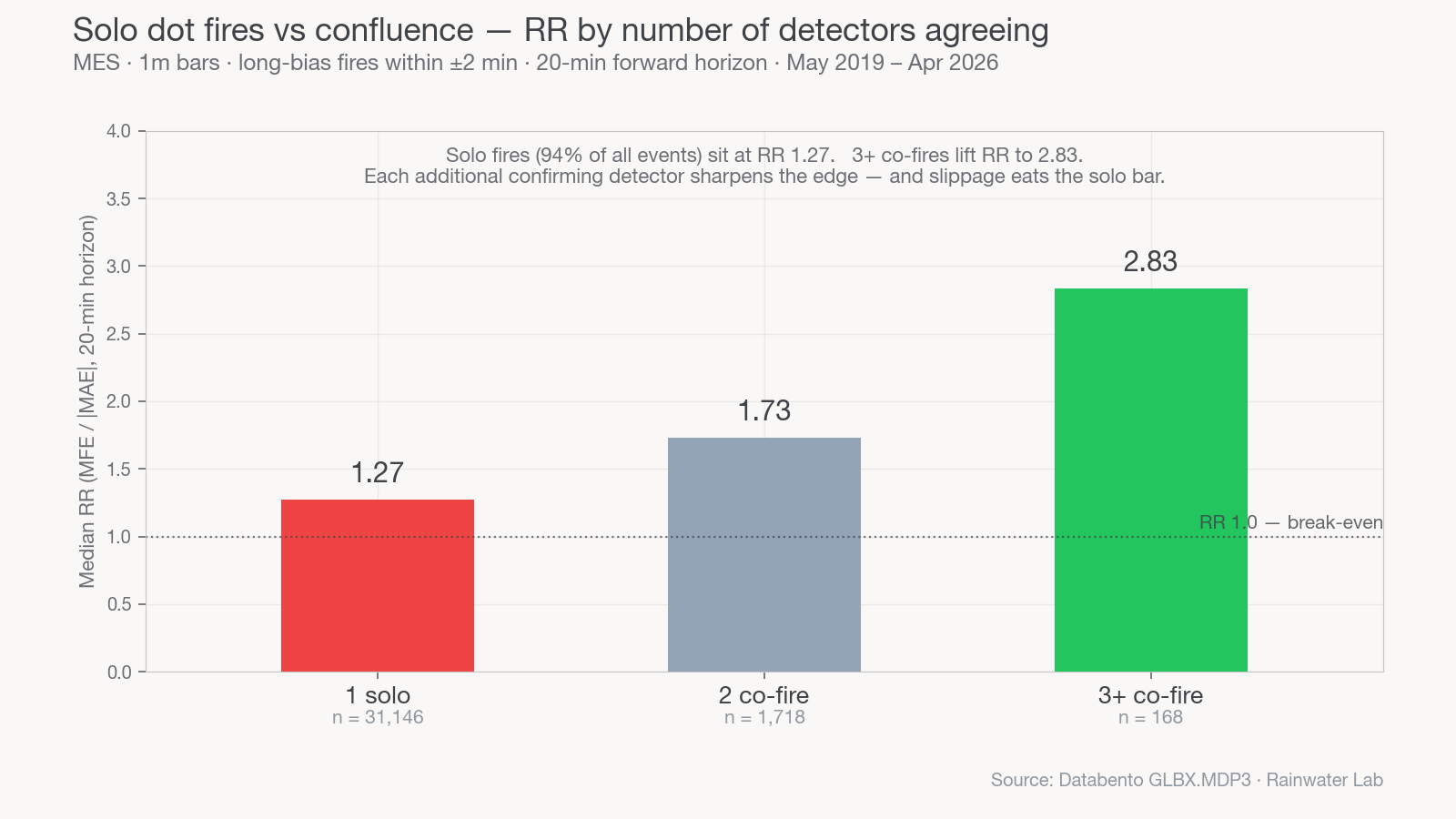

Solo dot fires

RR 0.50

After 12:30 ET

Edge collapses

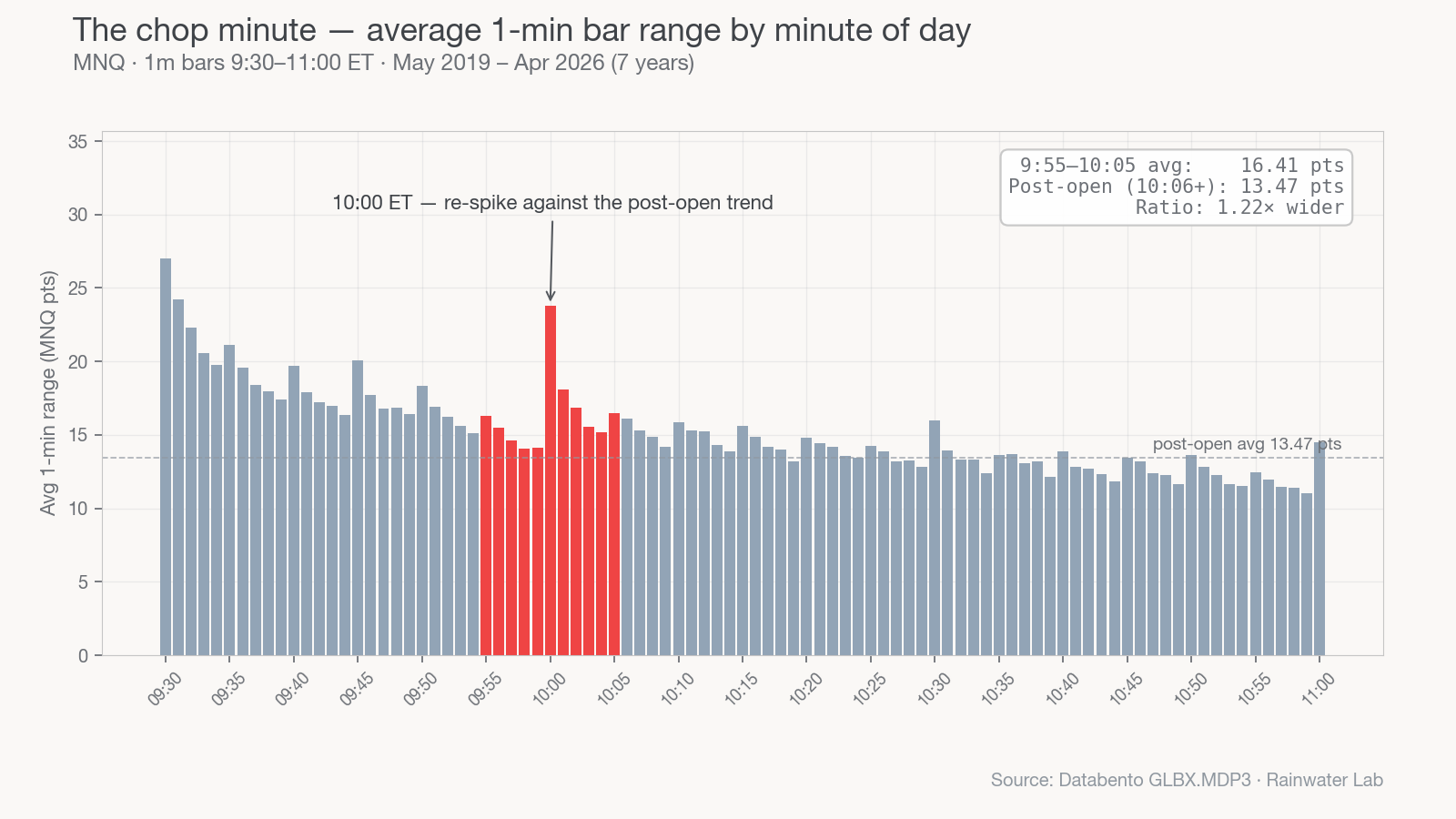

9:55 — 10:05

Widest 1-min range

The discipline paper

The previous paper was the optimistic one — the five setups that pay. This one is the mirror. Discipline is not the trades you take. It's the ones you skip. Every line in this paper is a setup that the seven-year dataset told us would lose us money or burn our concentration on a low-RR fire that crowds out a real one.

Saving money is making money. Every skip in this paper, on average, kept dollars in the account.

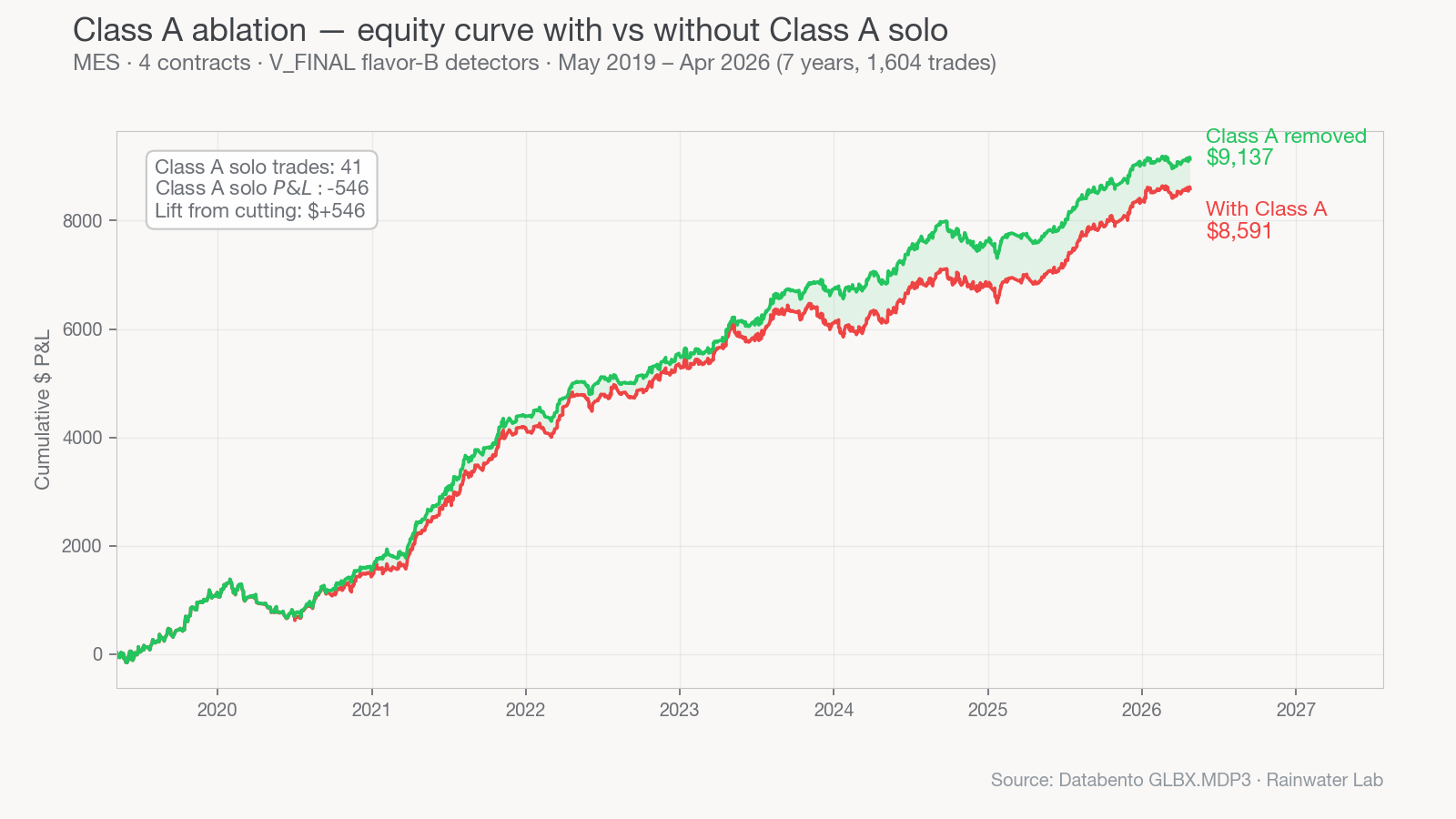

Class A — dropped

The legacy “Class A” structural pattern was inherited from earlier work and carried forward into V1 of the strategy because the win rate looked decent in isolation. When we ran it through the V_FINAL backtest with realistic slippage and the binary stop logic the rest of the strategy uses, it came out net-negative.

We considered every variant — softer stops, tighter targets, day-of-week filters, requiring co-confluence with another detector. None of them rescued the EV. The honest answer was: stop trading it solo. We did. The strategy got a measurable bump.

Solo dot fires — skipped

On the indicator, every detector firing on its own renders as a small gray dot — a marker, but not a marker that says “take this.” Across the dataset, single-detector firings cluster near break-even before slippage; once the round-trip spread is paid the median solo fire is sub-RR-1.0 net of cost. Two-detector co-fires push the bar to roughly 1.7. Three-plus to roughly 2.8.

The rule is hard: dot only, no marker label, no co-fire — pass. The discipline isn't philosophical. It's the difference between 64% WR with RR 3+ and 51% WR with RR 1.

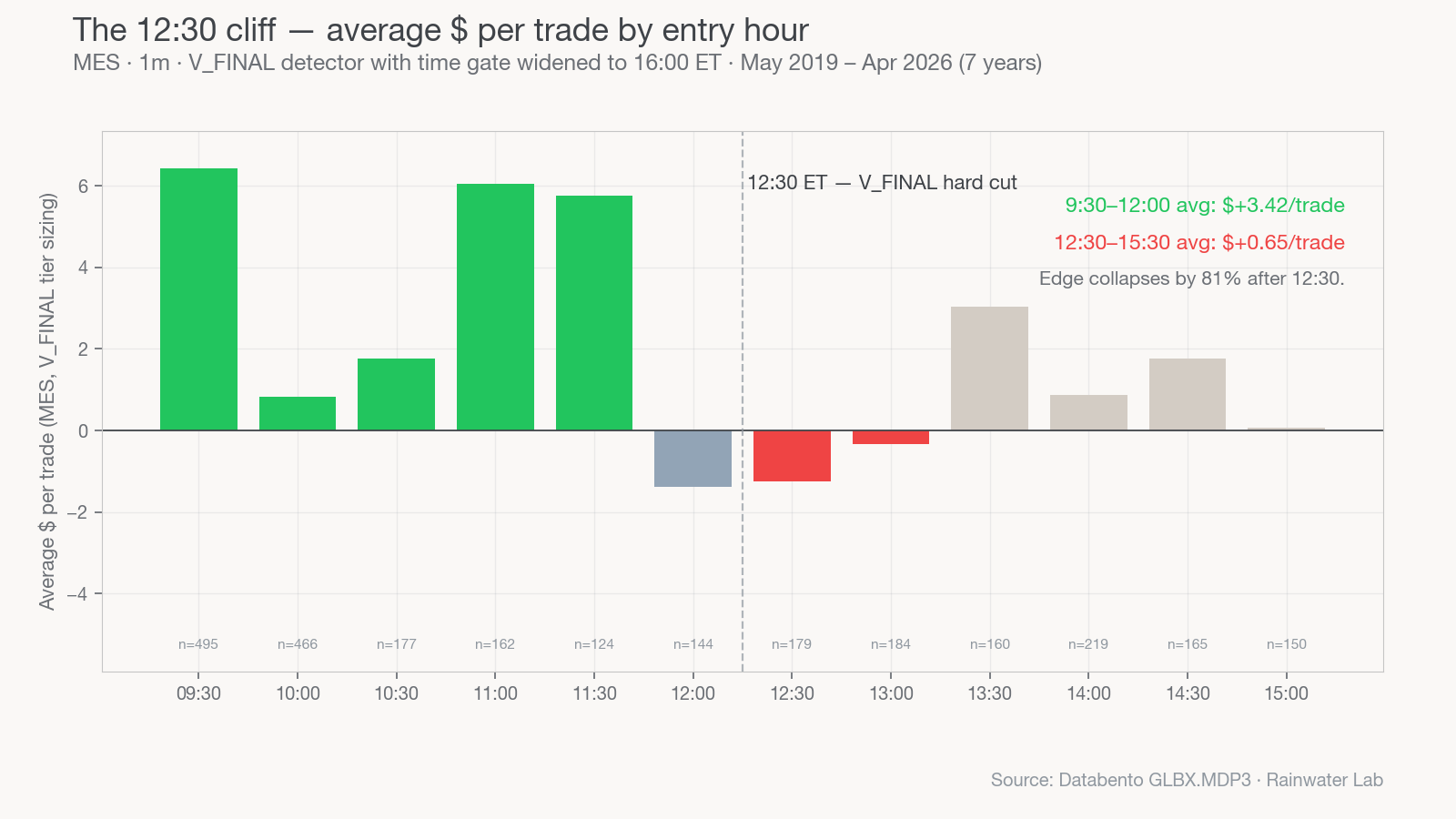

The 12:30 PM hard cut

9:30 – 12:30 ET

All edge

Where the strategy lives

After 12:30

Edge ÷ 5

Same detectors, no pay

Open positions

Close at 12:30

Unless trail is active

New entries

Never

After 12:30, period

We tested an afternoon module. We tested a 1:30–2:30 window. We tested an FOMC-day afternoon variant. None of them paid. The mid-afternoon hours look tradeable to the eye — they have movement — but the dataset is unambiguous: the kind of move that paid in the morning is structurally different from the kind that happens in the afternoon, and our detectors don't catch the afternoon kind.

The 12:30 cut is the single biggest discipline lever in the entire playbook. More subscribers will lose money trying to trade afternoons than will lose money on any single setup.

The 9:55 – 10:05 chop minute

The single widest one-minute range in the average trading day brackets 10:00 AM ET. On data days that's where the morning's economic prints land — CPI, retail sales, ISM. On regular days it's still where the morning's first impulse exhausts and the re-pricing happens. Either way, the bar is wide and the direction is random.

The rule is to not take new entries in the 9:55 to 10:05 ET band. If you're already in a trade and it's in profit, hold and let the trail manage it. If you're flat, you're flat until 10:05 unless something is so unambiguous that the rule's overhead would be silly to enforce on it.

Day-of-week filters

Tuesday — A+ tier only. The day-of-week skew finding (F4 in the master file) shows Tuesday's average up-day rate at roughly 50%, materially below Monday's 60%. The T2 confluence workhorse needs the underlying drift to make its math work. On Tuesday, that drift isn't there. Take A+ tier fires only.

Wednesday's first 30 minutes — skip. The first half-hour of Wednesday is the slowest, narrowest, most directionless window of the entire week, by a clear margin. The desk doesn't take entries before 10:00 ET on Wednesdays.

The cumulative effect

Take all four skip rules together — drop Class A, skip solo dots, hard 12:30 cut, chop-minute lockout, Tuesday/Wednesday filters — and the strategy moves from a marginal 51% WR / RR 1 system to a 64% WR / RR 3+ system. None of those filters add a setup. All of them remove ones that, on the data, didn't pay.

That's the whole insight of the discipline paper. The strategy is partially what it takes; mostly what it refuses to.

Futures waitlist

We're not running futures live yet. When we do, you'll be the first to know.

The research above is what we measure before we run a single dollar of subscriber money. Drop your email if you want first access when MNQ goes live on the desk.

Email only used for futures launch notifications. Unsubscribe any time.